In Your Debt: Forget the Fed, pay off your credit card debt

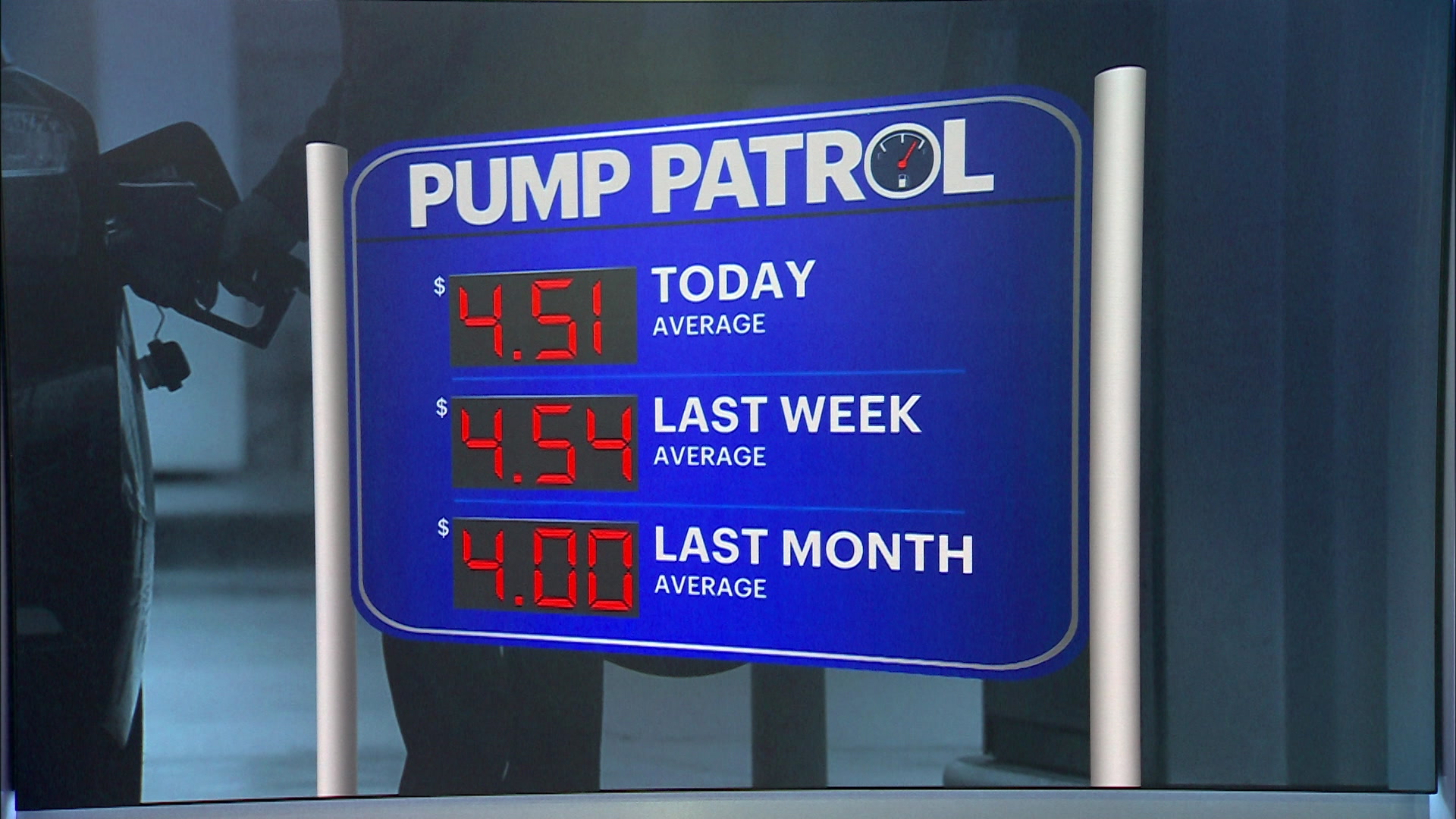

The cost of everything keeps creeping up. And if you happen to have credit card debt, that’s about to get a bit more expensive too, thanks to a series of interest rate increases beginning this month.

Share: